Kyle Prevost, editor of Million Greenback Journey and founding father of the Canadian Monetary Summit, shares monetary headlines and provides context for Canadian traders.

It was an enormous earnings week within the U.S. With so many unpredictable variables within the combine over the previous three months, many traders had been desperate to see what was truly happening beneath the hood of a number of the world’s largest firms.

IBM (IBM/NYSE): Displaying simply how panicky the market is in the intervening time, IBM kicked off the earnings bulletins this week with outperforming on each earnings and revenues, but the inventory worth dropped 4% in prolonged buying and selling on Monday. Earnings got here in at $2.31 per share (versus $2.27 predicted) and revenues at $15.54 billion (versus $15.18 billion predicted). Free money circulation was down from previous steering, with IBM stating that suspending enterprise in Russia was the principle wrongdoer.

Johnson & Johnson (JNJ/NYSE): Johnson & Johnson continued the sturdy earnings information pattern on Tuesday, asserting that even with sturdy U.S. greenback headwinds to battle, earnings had been $2.59 per share (versus $2.54 predicted) and revenues had been $24.02 billion (versus $23.77 billion). This excellent news was considered with skepticism by the market as JNJ was down in early buying and selling.

Lockheed Martin (LMT/NYSE): Protection large Lockheed Martin had a small earnings miss with an earnings per share determine of $6.32 (versus $6.39 predicted) and general revenues coming in at $15.45 (versus $16.05 predicted). Nevertheless, share costs traded up barely on the information that the Pentagon was ordering practically 400 extra F-35 fighter jets.

Tesla (TSLA/NASDAQ): Tesla reported a slight miss on revenues with $16.93 billion in complete gross sales (versus $17.1 billion predicted), however it got here out forward on earnings per share numbers with a formidable $2.27 (versus $1.81 predicted). Apparently although, Tesla determined to promote 75% of its bitcoin holdings throughout the quarter as properly.

Hmmm… Humorous that one didn’t make it into CEO Elon Musk’s Twitter web page. Tesla shares had been up barely in buying and selling after the quarterly name.

AT&T (T/NYSE): AT&T had maybe essentially the most noteworthy quarter of any firm that has reported earnings to date. Its shares instantly dropped 9%+ on Thursday morning. May unhealthy information set off such a fast sell-off, you would possibly ask? Effectively, the corporate added 813,000 month-to-month cellphone subscribers (considerably greater than the 554,000 predicted by analysts), and adjusted earnings got here in at $0.65 per share (versus $0.62 predicted). Revenues had been virtually equivalent to estimates, at $29.6 billion. Hidden from these uncooked numbers was the information that rising numbers of consumers weren’t paying their payments on time, and consequently, AT&T was forecasting $2 billion much less in free money circulation for the yr.

With earnings outcomes being fairly variable to date this quarter, it’s considerably tough to provide you with a one-size-fits-all concept. My main takeaway is that—regardless of continued strong earnings and gross sales numbers (for essentially the most half)—traders are undoubtedly wanting on the glass as “half empty.” They’re very anxious about what lies forward. Fund managers at the moment are extra pessimistic than they had been at any level within the final 20+ years.

Supply: BofA International Fund Supervisor Survey, as discovered on BNNBloomberg

Whereas making an attempt to foretell short-term market strikes is an effective method to make your self look fairly foolish, I can’t assist however assume there’s a good argument to be made for a long-term contrarian play in the intervening time. The broader market pattern was upward this week. However with investor sentiment nonetheless so low and valuation metrics reminiscent of price-to-earnings ratios persevering with to fall, I believe there might be some future traders thanking their present-day-selves for being grasping when everybody else was fearful in the summertime of 2022.

Need progress? Worth? Who cares, so long as it makes cash

Opposite to the bizarre “excellent news triggers mediocre market response” tales above, Netflix (NFLX/NASDAQ) was up round 7% in early buying and selling on Wednesday after revealing it misplaced one million subscribers within the final quarter. Gross sales income wasn’t fairly as sturdy as predicted, coming in at $7.97 billion versus a predicted $8.035 billion.

Many specialists pointed to the next as causes for traders’ optimistic reactions:

- Earnings per share had been as much as $3.20 versus a predicted $2.94

- Guarantees to cost extra for password sharing ought to enhance revenues

- The just lately introduced partnership with Microsoft to construct an ad-supported platform choice must also enhance revenues

- Netflix led of us to imagine subscriber numbers could possibly be down by as many as two million—so shedding “simply” a million didn’t appear so unhealthy!

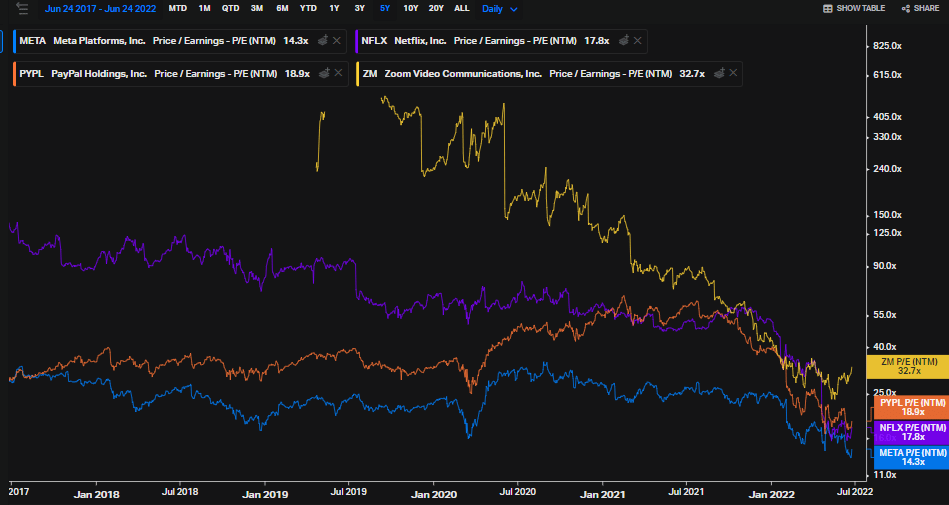

This might mark the start of traders taking a look at former “progress shares,” like Meta (META/NASDAQ) and Netflix, as mature firms that should be considered as revenue machines as an alternative of as purely progress engines.

All three MSOTM columnists (Dale Roberts, Jonathan Chevreau and myself included) have identified repeatedly that this isn’t the early 2000s when huge tech names had been “All sizzle and no steak.” Immediately’s tech firms would possibly nonetheless exist on-line and have nerdy CEOs, however they’re additionally extremely worthwhile.

Netflix and Meta (previously Fb) are so worthwhile, in reality, that given their current share worth meltdowns, they’re starting to be added to “worth inventory” lists and indexes.

What does this imply? They’re usually buying and selling at very low costs relative to their earnings and free money circulation. For instance, Meta’s free money circulation yield is above 8% proper now!

So even if you happen to hate the concept of Metaverse and imagine it’s only a large black gap of cash, the corporate is making greater than sufficient earnings to justify a considerable share worth enhance.

Equally, Netflix may stall and develop at a a lot slower charge going ahead. However so long as it might probably higher monetize its clients (opponents like Hulu have confirmed ad-supported fashions can work) and maintain their standing because the preeminent streaming service (possibly simpler mentioned than accomplished), then there should still be a shiny future for this firm.

Mature firms are likely to focus extra on the “much less attractive” subjects of value controls, upsells and maximizing buyer worth. Whereas this doesn’t drive funding information headlines the identical method “Hey, have a look at this shiny new factor that may take over the world!” does, it’s nonetheless a recipe for long-term monetary success.

Netflix and Meta are each accessible to Canadian traders through Canadian Deposit Receipts (CDRs), if you happen to’re on the lookout for a fast method to get portfolio publicity with out changing your Canadian {dollars} to U.S. Search for them at META/NEO and NFLX/NEO.

Air Canada’s journey to profitability is delayed… indefinitely

The current collapse of Air Canada’s (AC/TSX) skill to finish primary journey necessities, reminiscent of delivering folks on time, not shedding their baggage and/or usually making an attempt to again out of compensation to which shoppers are legally-entitled, has been properly documented.

What’s up for debate is whether or not all this unfavorable press will result in traders feeling any ache.

An argument could be made that Air Canada’s standing as an efficient monopoly in lots of areas, mixed with the ever-present authorities assist, means the corporate has a low threat of an entire meltdown. With Air Canada’s second quarter earnings report due within the subsequent couple of weeks, the inventory has been fairly unstable as traders wait to see simply how a lot the current turmoil has affected backside strains.

After just lately experiencing Air Canada’s companies, I’ve to say that I’m not in any respect assured within the firm’s skill to make the most of the current spike in journey demand. My spouse and I had been pressured to sleep on the ground at Pearson Airport final week (on account of baggage delays, crew delays, and upkeep delays) and had been subjected to a number of the rudest and most terrible customer support I’ve ever skilled. Now, in equity, the pilot and flight employees had been fairly nice {and professional}, and I’ve had a number of flawless flights with Air Canada over the previous couple of years. It could even be correct to say that we loved a minimum of the famous person skilled athlete expertise.

From an funding standpoint, we will let you know with a excessive diploma of conviction that we personally witnessed tons of of individuals swear off of flying with Air Canada for the foreseeable future. That’s going to have long-term repercussions which might be laborious to quantify in a quarterly report.

Should you’re contemplating “shopping for the dip” on Air Canada inventory, right here’s a couple of extra factors to contemplate:

- Air Canada’s 2022 first quarter resulted $900 million in adjusted losses, worse than 4th quarter of fiscal 2021

- Analysts are estimating much more losses for the second quarter (and their estimates had been overly optimistic in quarter one)

- Inventory worth is down 23% year-to-date

- Air Canada has $16 billion in debt and a $6 billion market cap

In additional optimistic airline information, Delta made headlines this week by asserting the acquisition of over 100 new plane from each Boeing and Airbus. Should you’re on the lookout for extra publicity to the entire airline sector (versus choosing winners and losers) you may want to try the JETS ETF. Air Canada makes up 2.61% of that ETF. Right here’s one tackle Canadian airline shares in 2022.

Celsius meltdown continues destruction of the crypto facade

One other of the crypto world’s huge names declared chapter this week. Crypto lender Celsius was pressured to confess that despite the fact that it was said as just lately as October, 2021 that the corporate had $25 billion price of belongings underneath administration, it was now all the way down to having solely $167 million money readily available.

Following a pointy decline this yr, the worth of some cryptos recovered barely this week. Do you propose to purchase any cash forward of a possible rebound?

— MoneySense (@MoneySense) July 21, 2022

Having $167 million money readily available is a matter if you owe customers $4.7 billion!

In fact, the information has been stuffed with studies of varied cryptocurrency-based firms operating into monetary troubles and shedding workers. Fears of a “contagion impact” proceed to plague your complete crypto ecosystem.

It’s virtually as if there aren’t any underlying fundamentals for the asset to fall again on when funding sentiment sours.

Naturally—in true crypto trend—Bitcoin’s worth realized a slight restoration regardless of the unfavorable information. I’ve now come round to the conclusion that the bitcoin fanatics are each bit as religiously dedicated to their embrace of this asset as “gold truthers” are to their “treasured.”

This implies there’ll all the time be room for speculators to generate income. It additionally signifies that it’s not an funding.

Except for a really slim utilization case to be made by black markets and residents of badly failing economies like Venezuela, there continues to be no underlying motive to own bitcoin. Given the previous few months, one fantasy we will safely say is busted is that inflation would quickly make the U.S. greenback nugatory and reveal the power of cryptocurrencies as “inflation fighters.”

Whereas I’m fairly sure such small utilization instances don’t justify a valuation of USD$20,000+, I’m virtually as sure that the mixture of leveraged speculators (trying to capitalize on “The Larger Idiot”) and zealot-level “HODLers” will trigger bitcoin and different cryptocurrencies to spike once more.

If the worth on particular crypto currencies spikes within the months to return, current traders (say from the final two years) might be introduced with an fascinating choice now that they’ve skilled simply how unstable the funding could be. It’s one factor to know in concept your funding can shortly drop 70%+, however it’s one other to look at it occur to your account. Whether or not these traders determine to promote their cash and breathe a sigh of aid as they break even, or double down on their crypto convictions stays to be seen.

No matter short-term actions, the lightning pace with which so many of those crypto firms have gone from grandiose statements about world domination to subdued company capitulation has revealed simply how a lot uncertainty is inherent on this obscure “asset class.”

Kyle Prevost is a monetary educator, writer and speaker. When he’s not on a basketball courtroom or in a boxing ring making an attempt to recapture his youth, yow will discover him serving to Canadians with their funds over at MillionDollarJourney.com and the Canadian Monetary Summit.

The publish Making sense of the markets this week: July 24 appeared first on MoneySense.