Common RESP contributions have the extra advantage of dollar-cost averaging: investing equal quantities of cash at common intervals (say, as soon as a month) as an alternative of bigger lump sums much less usually (say, annually). This decreases market threat and smooths returns over time. Let’s run some numbers utilizing a simplified instance. In case you have been to contribute $2,500 yearly, you’d attain the $7,200 CESG restrict within the RESP’s 15th yr. The $50,000 contribution restrict might be reached by making a much bigger contribution—$7,500—in yr 18. Assuming a 6% common price of return, the ultimate RESP account steadiness could be $101,514: $50,000 from contributions, $7,200 from the CESG and $44,314 from funding earnings.

Liut’s tackle this method: “This can be a nice possibility for many individuals who don’t have more money to contribute upfront however need to maximize the CESG. For individuals who have additional non-registered funds, nonetheless, I’m usually requested if a lump-sum contribution is one of the best method.”

Subsequent, we’ll discover utilizing a lump sum to front-load an RESP.

Possibility 2: Entrance-load the utmost RESP contribution

Few households can have the flexibility to contribute the utmost $50,000 in yr one, and this method additionally carries the chance of markets slumping quickly after investments are bought. Nevertheless, it’s price contemplating this selection to see the potential advantages of getting investments tax-sheltered early.

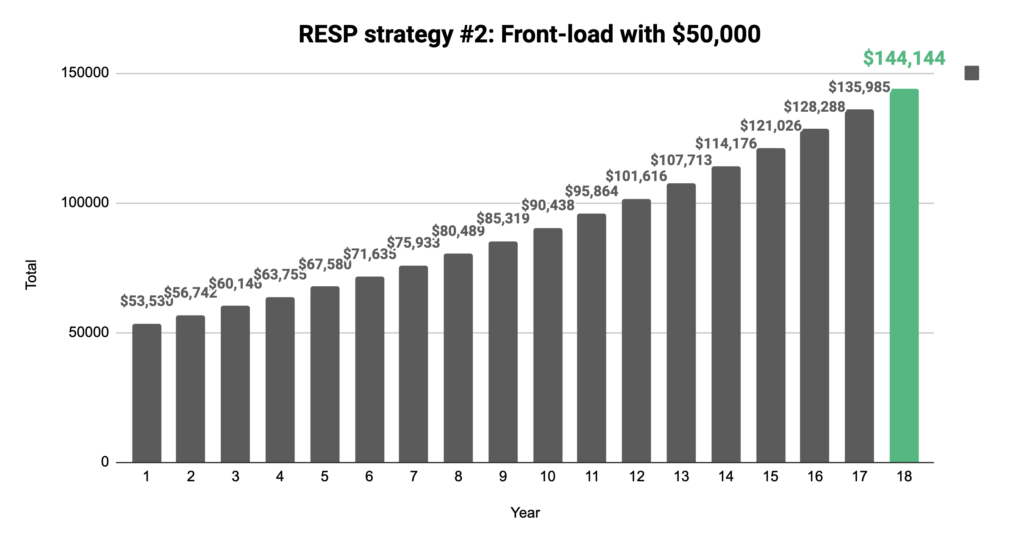

Contributing the utmost $50,000 in yr one would solely end in $500 of CESG. Alternatively, all that cash can develop tax-free for the total 18 years. For illustration functions, assuming a 6% common price of return as in our first instance, front-loading with $50,000 would end in a last steadiness of $144,144: $50,000 from contributions, $500 from CESG and $93,644 from funding earnings.

So, we’ve our reply, proper? Not so quick.

Disadvantages of front-loading an RESP with a big lump sum

Although front-loading seems to be a greater technique than possibility 1 due to the upper total return, right here’s why it’s not: It ignores the truth that if the $50,000 had not been used to fund the RESP, it may have been invested elsewhere. These funding returns, significantly if they’re acquired inside a tax-sheltered account like a TFSA or RRSP, would negate the good thing about front-loading. To be useful, any lump-sum contribution should come from funds out there after RRSPs and TFSAs have been maxed out.

“The advantage of lump-sum RESP contributions is absolutely to maneuver funds right into a tax-sheltered account as early as potential,” says Liut. “So, it solely works if the opposite registered accounts are already being maximized.”