Kyle Prevost, editor of Million Greenback Journey and founding father of the Canadian Monetary Summit, shares monetary headlines and provides context for Canadian buyers.

Banking on stability and warning

Canadian buyers love their banks. Yr in and yr out, banks present reliable dividend development and strong long-term share value will increase as nicely. In addition they make up an enormous a part of any Canadian index fund, in addition to the majority of Canadian pension funds.

So, when the banks pull again the curtains to disclose how enterprise is doing, we take discover.

With a set of combined outcomes, the principle takeaway seems to be that the Large 6 (BMO, CIBC, Nationwide Financial institution, RBC, Scotiabank and TD) regarded on the financial storm clouds on the horizon and determined to batten down the hatches.

By provisioning extra of their earnings for default loans, the information wasn’t nearly as good as current earlier quarters. That stated, these conglomerates proceed to tick alongside cautiously, dependably spinning off free money movement.

Large financial institution earnings for Q3 2022

All numbers are in Canadian {Dollars}.

Financial institution of Nova Scotia (BNS/TSX): In a unfavourable begin to the week, the Financial institution of Nova Scotia barely missed expectations as adjusted earnings rose 4% from final yr, however nonetheless got here in at $2.10 (vs $2.11 predicted). Scotiabank said it’s setting apart $412 million for loss provisions, up from $219 million final quarter. Nervous buyers triggered the inventory to sink greater than 5% on Tuesday after the earnings name.

Royal Financial institution of Canada (RY/TSX): Warning that “the tip of an financial cycle is close to,” RBC additionally misplaced some revenue on account of growing mortgage reserves. Its third quarter revenue was down 17% from final yr. RBC’s adjusted earnings per share had been $2.55 per share (versus $2.66 predicted). Shares had been down 2.6% on Wednesday after earnings had been reported.

Nationwide Financial institution of Canada (NA/TSX): Nationwide Financial institution did comparatively nicely with a slight adjusted earnings per share beat of $2.35 per share (versus $2.34 predicted). Its Canada-based enterprise was up considerably, however its worldwide models did drag down outcomes to some extent. Even with the slight beat, shares of NB completed Wednesday down practically 1%, because of the broader development in Canadian financials.

Toronto-Dominion Financial institution (TD/TSX): TD additionally topped earnings expectations, coming in at $2.09 per share (versus $2.04 predicted). Canada’s second-largest financial institution benefitted from 11% development on its U.S. retail banking section. Shares completed up 0.74% on Thursday after reporting.

Canadian Imperial Financial institution of Commerce (CM/TSX): CIBC adopted go well with and in addition introduced a slight beat on Thursday, ending the quarter with earnings per share of $1.85 (versus $1.82 predicted). Very similar to the opposite banks, CIBC’s steering prominently talked about elevated mortgage loss provisions. Shares completed the day down 0.20% on the day regardless of the constructive earnings information.

The Financial institution of Montreal (BMO/TSX) might be reporting its quarterly outcomes subsequent Tuesday.

Whereas the banks’ concern for the financial future is definitely among the strongest proof I’ve seen but for robust recessionary issues, I imagine the collective data we garnered from the earnings name is usually excellent news. By and enormous, the Canadian banks continued to do fairly nicely on a pre-tax pre-provision foundation, and are benefiting from robust retail banking performances.

Given their respective valuations, I believe they’ve so much to supply buyers in a unstable setting. The loan-loss provisions would possibly become useless preparation for a wet day—through which case the banks will simply unwind these reserves to the advantage of shareholders. If the uneven financial waters do start to sink a number of boats, the banks could have but once more earned their popularity as cautious and secure operators. Try my article on MillionDollarJourney.com for extra on Canadian financial institution shares.

Rates of interest proceed to draw… curiosity

“Don’t struggle the Fed” grew to become some of the repeated aphorisms of the final decade, when it got here to predicting long-term inventory market returns. The concept that the Federal Reserve would decrease rates of interest to maintain the financial system buzzing (and inventory valuations excessive) was seen by some as a digital assure of future returns.

Now that the financial occasion has gotten too scorching, the Fed is shifting in the other way—making an attempt to remove the punch bowl. The query now’s: Simply how exhausting is The Fed going to struggle? Additionally, how a lot of a resistance does the market need to put up?

Consequently, the world’s financiers tuned on this week to listen to what Federal Reserve Chair Jerome Powell would reveal concerning the central financial institution’s long-term prognosis.

It seems that whereas the overwhelming majority of forecasters had been predicting a increase in the important thing price, the controversy was between a 0.50% increase and a 0.75% increase. Whereas these modest hikes may not look like a giant deal to most, they will have fairly substantial results on the valuation of most property. Bond yields gave the impression to be baking in a extra aggressive Fed posture—at the very least within the brief time period.

In different rate of interest information, China reduce charges final week, once more, after slicing them solely two weeks beforehand. This shock transfer is a transparent indication that China’s central financial institution is turning into increasingly more fearful a few attainable actual property collapse. Many market forecasters predict development projections for the Center Kingdom of a mere 3% this yr—a far cry from the 5%-plus development charges which have characterised its financial system the previous few a long time. The Yuan continues to undergo versus the U.S. greenback because of these cuts.

Supply: Google Finance

Lastly, the gloomy information out of the U.Ok. was that merchants are betting their rates of interest might be compelled as much as 4%, as they attempt to battle intense inflation expectations of as much as 18%.

American shoppers aren’t tapped out but

On the heels of final week’s mega-cap retailer studies, this week noticed a number of area of interest retailers report their outcomes from the final three months. All figures under are in U.S. foreign money.

Dicks Sporting Items (DKS/NYSE): Earnings per share got here in at $3.68 (versus a predicted $3.58), and revenues had been $3.11 billion (versus $3.07 billion predicted).

JD.com (JD/NASDAQ): Earnings per share had been reported at $4.06 (versus a predicted $2.78), and revenues of $267.6 billion (versus a predicted $263 billion). Be aware that JD.com is a Chinese language ecommerce website usually in comparison with Amazon, and is traded on the NASDAQ trade by way of ADR.

Nordstrom (JWN/NYSE): Earnings per share had been $0.81 (versus a predicted $0.80), and revenues had been $4.1 billion (versus a predicted $3.97 billion).

Macy’s (M/NYSE): Earnings per share had been a beat at $1 (versus a predicted $0.85), and revenues had been $5.6 billion (versus a predicted $5.49 billion).

City Outfitters (URBN/NYSE): Incomes per share missed at $0.64 (versus a predicted $0.67) and, it posted revenues of $1.18 billion (versus an estimate of $1.16 billion).

Whereas these are 5 very totally different retailers, we see that, broadly talking, the retail traits signaled final week maintain true. Stock pressures are forcing markdowns, and inflationary prices are compressing margins. That stated, folks do have jobs and are shopping for merchandise. The patron sky isn’t falling.

GM funding pays dividends, actually

Basic Motors (GM/NYSE) made the headlines this week when it reinstated its quarterly dividend, in addition to saying a USD$5 billion inventory buyback. (Figures under are in U.S. {dollars}.) GM shareholders will get $0.09 per share every quarter going ahead.

Whereas this isn’t even near changing the $0.38 per share GM shelled out earlier than it suspended its dividends in 2020, it’s a nice vote of confidence within the firm’s potential to create free money movement going ahead. The dividend yield for the inventory now stands at 1%. GM inventory value was up about 4% on the information, however remains to be down about 33% this yr.

GM CEO Mary Barra adjusted expectations by stating that whereas GM would “contemplate all alternatives to return extra capital to shareholders,” the majority of the corporate’s capital could be reinvested into {the electrical} automobile focus GM could have going ahead. GM, together with all different conventional carmakers, remains to be the race in opposition to Tesla for scale. Tesla must handle manufacturing capability and distribution fashions. GM wants to determine its battery and efficiency know-how.

I’m undecided who will win this automotive race, however I do know that Tesla’s inventory stays priced for absolute good execution, whereas the market has not prolonged practically the identical good thing about the doubt to GM, Ford, and others. Tesla is little doubt hoping that their 3-for-1 inventory break up this week will outcome within the standard increase to total market capitalization.

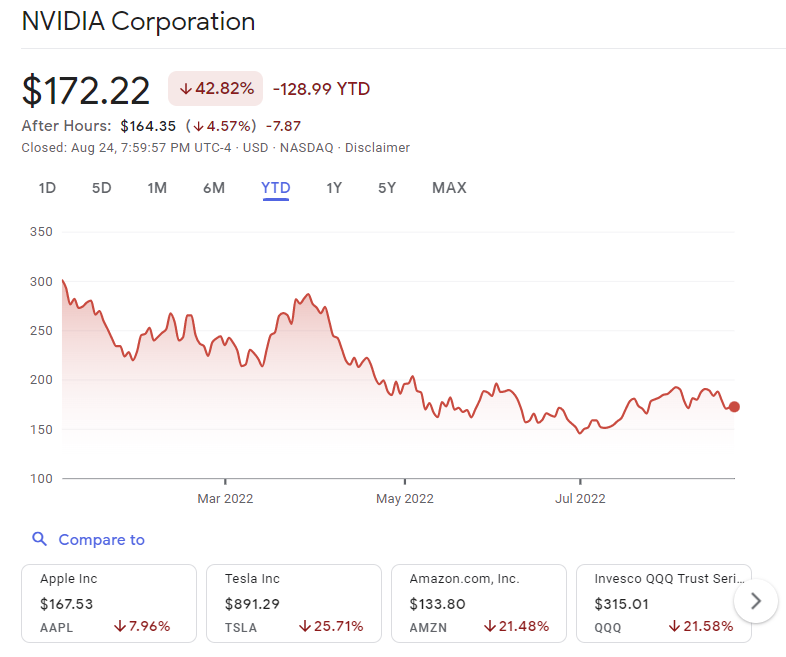

Nvidia’s not taking part in video games

Whereas most of the large American tech names are fairly well-known to Canadian buyers, I discover Nvidia (NVDA/NASDAQ) usually flies underneath the radar. Whereas the corporate is considerably smaller than Apple or Amazon, it’s nonetheless greater than 3 times larger than RBC (Canada’s largest firm).

Nvidia introduced its earnings this week, and whereas expectations had already been lowered, the {hardware} big nonetheless missed on projected revenues and earnings. Earnings per share got here in at solely $0.51 (versus $1.26 predicted) and revenues had been USD$6.7 billion (versus USD$8.10 billion predicted).

Gross sales had been harm largely on account of a 33% fall in its gaming vertical and in addition to a decreased demand for graphics playing cards. Some commentators speculated that almost all of the demand for Nvidia’s high-end graphics playing cards had been from cryptocurrency miners than beforehand thought.

Given the scale of the miss, I’m stunned to see the inventory value down solely 4.5% in after-hours buying and selling. Nvidia is now down virtually 43% on the yr, which simply goes to indicate how rapidly the demand for {hardware} has dropped after the pandemic’s spending binge.

Kyle Prevost is a monetary educator, creator and speaker. When he’s not on a basketball courtroom or in a boxing ring making an attempt to recapture his youth, you’ll find him serving to Canadians with their funds over at MillionDollarJourney.com and the Canadian Monetary Summit.

The submit Making sense of the markets this week: August 28 appeared first on MoneySense.