For homeowners of a privately restricted firm, does this sound acquainted?

- Have you ever not contributed totally to your £40,000 pension annual allowance in the course of the present or newest three tax years?

- Do you’ve got a tapered Annual Allowance?

- Do you’ve got a low-level wage and high-level dividends?

- Do you’ve got important headroom below the Lifetime Allowance?

- Is the corporate capable of make massive contributions from both money or surplus earnings?

- Does your corporation have important ranges of retained earnings?

- Do you want to buy business property as an funding or to commerce from?

With tax charges rising and allowances being frozen, homeowners of their very own non-public restricted firm could have a decreased means and willingness to attract earnings from their firm. As such, retained earnings can languish in money deposits, incomes little curiosity in opposition to a excessive inflation backdrop, risking a possible lack of a number of tax allowances or challenges throughout a enterprise sale.

It looks like a no-win scenario ……………. or is it?!

Nicely, not fairly. With a sturdy monetary & tax planning technique, returns on property and tax financial savings will be made.

Contributing to a pension is a well-known motion to most, however it’s digging deeper into outlined profit or outlined contribution preparations which may broaden planning potential.

Outlined Contribution (DC) pensions are predominantly private pensions, SIPPs and SSASs and these are the commonest pensions with self-employed people or people within the non-public sector. Outlined Profit (DB) pensions are nonetheless prevalent within the public sector, however this fashion of pension isn’t just unique to the NHS or Hearth Service…

Cue the Outlined Profit SSAS (DBSSAS).

A DBSSAS advantages from the identical options as a Outlined Contribution SSAS (DCSSAS), nonetheless, the first variations are how the ultimate pension is calculated and the way contributions are funded and assessed for the aim of a person’s Annual Allowance (AA). Which means that there may be probably considerably higher scope for the corporate to contribute to a DBSSAS, than there can be to a DC scheme.

DC pensions obtain contributions both gross or internet of tax. The restrict for tax aid (AA) is usually £40,000 pa (this can be decreased for sure people).

The contribution to DB pensions then again, is calculated by accounting for the rise in advantages in the course of the pension 12 months. Let’s assume a DB pension gives an earnings for a person of £2,500 pa. HMRC multiply this by 16 to find out how a lot of the AA has been used.

| DCSSAS | DBSSAS | |

| Technique of Annual Allowance evaluation | Contributions acquired | Profit accrual |

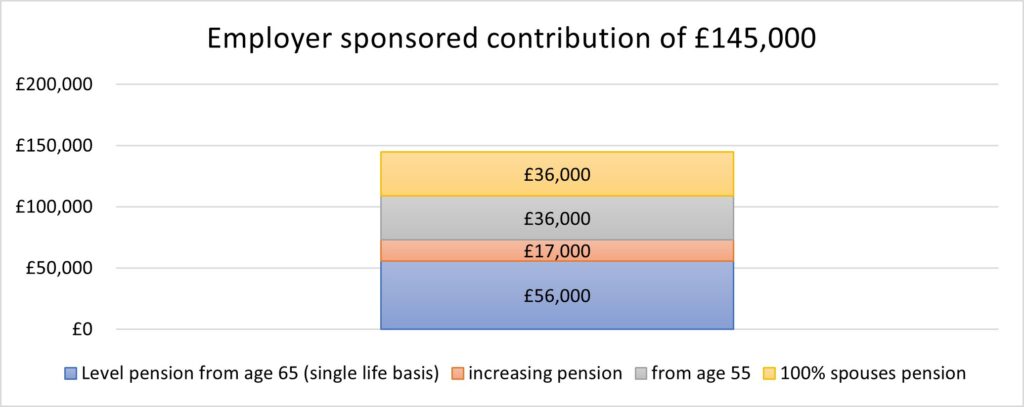

| Most annual profit | Annual Allowance (2022/23) £40,000 | Annual pension of 1/16th of the Annual Allowance £2,500 Price to an employer to fund (as much as £145,000) |

The query due to this fact is what does a pension like this price to fund? The reply to this may be “rather a lot”!

A pension actuary calculates what funds are required to ship the goal earnings together with different advantages resembling inflationary will increase, widows’ pensions and different ensures.

Enhancements to a person’s advantages are pricey, consequently, the contributions actuarially calculated to supply such a pension are significantly higher than the £40,000 as a financial quantity to the sponsoring employer. In precept, right here’s the way it works:

Values used within the examples on this article are for illustrative functions solely and shouldn’t be construed as a personalised suggestion. No motion needs to be taken with out searching for additional formal recommendation.

Your private circumstances and due to this fact your means to utilize a DBSSAS pension association, contributions and tax reliefs will range from particular person to particular person.

Must you want to focus on DBSSAS additional, and discover out whether or not or not it could be appropriate on your circumstances, please contact Robin Houghton (rob.houghton@mooreandsmalley.co.uk).