There are numerous monetary professionals who name themselves monetary planners. Everybody from insurance coverage salespeople, funding brokers and managers or CPAs who dabble with planning name themselves monetary planners. For higher or worse, all the aforementioned professionals have helped to form our purchasers’ minds and expectations of monetary professionals. And consequently, many purchasers assume they’ve holistic monetary plans, however they really don’t.

The purchasers of many CPA companies usually lack somebody who acts as their monetary head coach, steering them via the inevitable twists and turns to be encountered of their monetary and private lives. Most of those twists and turns have a mess of attainable penalties and actions. Finally, the alternatives that really feel greatest to your purchasers will usually come from a holistic evaluation of all of the monetary and private penalties.

As a consumer’s accountant, you could have good perception to their private monetary affairs. You see their sources of earnings, their deductions, find out about their household and may simply get a glimpse into some areas that want consideration. From school financial savings to the possession of rental or enterprise property, the CPA viewpoint stands out as the broadest and deepest view that any of the purchasers’ different professionals have. For the accountant trying to construct deeper relationships with fewer, higher purchasers, recognizing open points within the monetary lives of your purchasers is an efficient begin. The connection strengthens even additional when you’re part of the answer to assist get these points solved, reasonably than barking out orders and delivery them off to another person to get the job executed.

Accountants have chosen to serve purchasers in two methods relating to their monetary plan. Some select to not instantly present holistic planning companies and function an overseer and spring into motion when requested. These practitioners might refer their purchasers to different advisors and the consumer will get a staff of pros who might or might not likely coordinate their recommendation to lead to a holistic plan. To those that choose this much less lively function, the stability of this text will show what kind of companies your purchasers ought to be getting. It should assist you to be a greater useful resource for them as you contribute wanted experience to the planning course of for the household.

All of the transferring components

Holistic planning takes much more time than merely working numbers and doing retirement forecasts. Holistic planning includes full consideration of all of the transferring components in your purchasers’ lives. It begins with money circulate at the moment and sooner or later. Some purchasers have a transparent imaginative and prescient for his or her future earnings or investments and others are nonetheless within the constructing section the place earnings and their future portfolio worth aren’t sure. Some may have hands-on assist with saving, budgeting and spending, particularly on the qualitative facet.

Serving to a consumer to visualise their superb retirement by way of how they’ll spend their 168 hours per week could be a magical expertise for them. Shoppers get so hung up on the cash points that many by no means actually take the time to think about their superb day(s). The information of the planning skilled can then assist quantify the price of these visions and perceive what it can take financially to make that occur below a variety of prospects and situations, after which talk that successfully to the planning staff and the purchasers. All choices have measurable penalties, however it’s the qualitative discussions that always drive most quantitative choices.

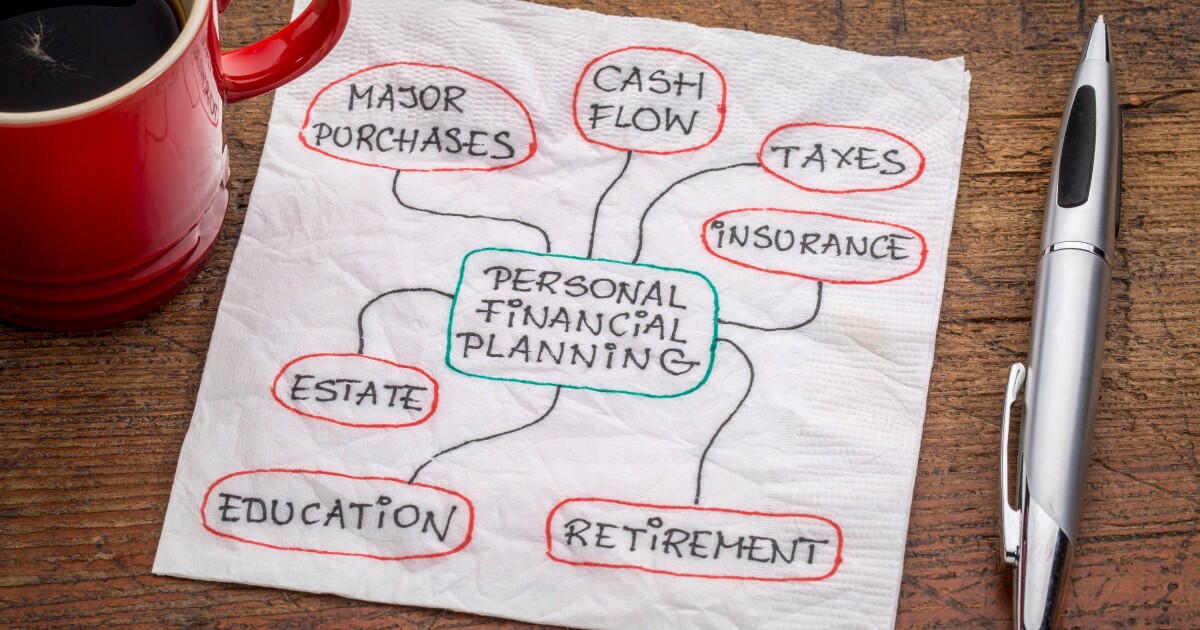

private monetary planning idea – serviette doodle with cup of espresso espresso

MarekPhotoDesign.com – inventory.ado

Past money circulate and incorporating a consumer’s imaginative and prescient into the planning, a holistic plan should embrace evaluation and steering on some particular monetary areas. These areas are particularly danger administration, funding recommendation, tax planning, retirement planning and property planning, household governance, and enterprise and succession planning. Past these necessary cornerstones of the holistic planning course of, client-specific topic issues might also want consideration. These points might embrace schooling planning, particular wants planning, aiding with elder mother or father points or any difficulty that can hamper or help a consumer to perform a objective and stay their imaginative and prescient.

Threat administration, in my view, could also be one of many largest gaps in lots of a consumer’s monetary image. Except a planner is dedicated to holistic planning, the danger administration space incessantly will get a reasonably mild assessment service from advisors. A holistic strategy to danger administration would ask the final query: What can occur to mess up this image?

A holistic danger administration strategy would begin by analyzing the areas of danger in your purchasers’ lives. Most individuals have houses and automobiles, and it isn’t sufficient for a monetary planner to counsel {that a} consumer converse with their property and casualty agent to see if their protection is ample. The holistic planner should assessment these contracts and confirm if the protection is ample, an excessive amount of or too little, and that it’s supplemented with needed add-ons for catastrophic legal responsibility or particular property.

An analogous danger evaluation ought to be carried out on the enterprise facet of the consumer’s life. This space is one the place some planners don’t have the schooling or expertise to carry out on the highest stage, however it nonetheless must be executed. A mature ensemble observe in all probability has that experience in-house. If not, that doesn’t imply which you can ignore the subject; a holistic planner should discover the experience to ensure that the consumer shouldn’t be uncovered to unknown or unprotected dangers.

A holistic danger evaluation will get past the insurance coverage and addresses retention and mitigation methods as properly. This would come with a dialogue of how the property (private or enterprise) is owned and if there are companions or different homeowners who might materially add to your consumer’s dangers resulting from historical past or expertise.

Past investments

Due to the investment-only mentality of many monetary professionals over the many years, many purchasers assume that investing is wealth administration. After all, investing is one a part of the numerous transferring components to a holistic plan, however hardly essentially the most vital. A holistic plan to your consumer’s portfolio contains understanding the vacation spot, an evaluation of their present holdings after which a advice to convey their portfolio to a extra optimum place if wanted. This plan ought to deal with time, danger tolerance and the opposite sources accessible to a consumer. However past the fundamentals of portfolio design, the holistic planner should take note of tax penalties, possession points and beneficiary elections to the extent that the funding is held in a belief, retirement plan or an insurance coverage product.

Accountants know higher than anybody that tax planning is a year-round endeavor, and never some magic wand that you just wave on tax day. Particularly in mild of current tax modifications and the upper marginal brackets for high-income taxpayers, taxation is starting to assist drive choices once more within the minds of your purchasers. The holistic planner can have a great understanding of a consumer’s tax state of affairs, but supply proactive methods to cut back that invoice going ahead. The reductions might come on account of the timing of earnings and deductions, creating deductions or just including some tax alpha or asset location evaluation to the funding course of.

Retirement planning includes greater than letting the consumer know the way a lot cash they’ll must get pleasure from a snug retirement. It could entail going again to the consumer’s imaginative and prescient for his or her future way of life and serving to to get there or aiding with what must be executed to get there. Generally, the reply requires robust love and also you’ll need to let the consumer know that their targets are unrealistic, and that they might must make extra or spend much less. At a minimal, retirement planning wants to incorporate a forecast below just a few completely different situations, and evaluation of retirement earnings choices from Social Safety and/or pensions, and common monitoring to see that spending, investing and earnings haven’t strayed too removed from the unique forecast.

For purchasers who personal a enterprise, the holistic advisor will coordinate a plan for serving to to design the suitable retirement plan for a enterprise proprietor that may meet their accumulation objectives and supply efficient tax planning.

The place there’s a will …

I’m all the time shocked by the variety of individuals strolling round with an outdated or no property plan. It’s simple to see why this space is so problematic. Few individuals actually wish to step up and speak about their demise. This material turns many purchasers off. Some purchasers assume that an previous will is healthier than no will and their present solid of pros doesn’t appear to be too involved in regards to the lack of high quality paperwork.

Many planners do a cursory job telling purchasers that they want new wills and that they need to think about trusts, sturdy powers of lawyer and well being care directives. With all due respect, a consumer doesn’t must pay a planning price to be taught that. What a holistic planner does for an property plan is focus on the choices, from easy wills to trusts and guarded entities. The holistic planner has the chance to speculate the time with a consumer to ensure that they perceive their property plan and make choices that can swimsuit their wants at the moment and the wants of their heirs that will span for generations. These discussions get very private and ought to be particular sufficient to seek out out greater than merely who will get what after they cross. Your discussions will likely be in regards to the maturity and way of life of heirs (sure, even grownup kids), how property are held for any surviving spouses, asset safety, beneficiary elections, selection of trustees, and take care of the potential remarriage of a partner.

When an property is sophisticated with second marriages, kids from multiple marriage or particular wants conditions, the conversations get very attention-grabbing. For a lot of purchasers, this can be the primary time of their lives that they’ve been requested about accommodate and plan for these nuances.

Holistic planning shouldn’t be the service delivered by many who name themselves monetary planners. Some are too lazy. Others lack the information or the dedication to their purchasers. However as talked about earlier than, purchasers’ perceptions of the planning course of could also be restricted to what they’ve seen and heard earlier than. It’s as much as you to alert them about the advantages of addressing these points on a complete foundation.

The excellent news is that I consider {the marketplace} is altering. Individuals are sick of getting bought stuff and getting bought a invoice of products in regards to the complete or holistic companies {that a} sure planner claims to ship. Because the accountant, you might be in a great place to see that their wants are met or that you just introduce them to a planner who’s and able to delivering that holistic plan.